Could Your Money Be Losing Value? 9 Smart Financial Strategies to Stay Ahead of Inflation and Build Lasting Wealth

Category: Personal Finance

Tags: Personal Finance, Inflation, Money Management, Wealth Building, Financial Planning, Budgeting, Investing, Saving Money, Emergency Fund, Retirement Planning, Financial Literacy, Passive Income, Smart Investing, Long-Term Wealth, Economic Trends

Could Your Money Be Losing Value? 9 Smart Financial Strategies to Stay Ahead of Inflation and Build Lasting Wealth

Money sitting safely in a bank account may feel secure, but over time inflation can quietly reduce what those savings can buy. As the cost of housing, groceries, healthcare, transportation, and everyday necessities changes, many families are realizing that simply saving money may not be enough to preserve long-term purchasing power.

Financial experts often point out that successful money management is about balancing security with growth. Maintaining emergency savings remains essential, but building wealth usually requires a thoughtful strategy that includes budgeting, investing, debt management, and long-term planning.

No financial plan is guaranteed to eliminate risk, and every person’s circumstances are different. However, developing healthy financial habits can improve resilience during uncertain economic conditions and help prepare for future opportunities.

Here are nine practical financial strategies that may help strengthen your financial future.

1. Understand How Inflation Affects Everyday Life

Inflation refers to the gradual increase in the prices of goods and services over time. Even moderate inflation can reduce purchasing power if income and savings fail to keep pace.

For example, groceries, utility bills, travel costs, and housing expenses may become more expensive over several years. Understanding how inflation affects your budget allows you to adjust savings goals and spending habits more effectively.

Rather than fearing inflation, use it as motivation to review your financial plan regularly.

2. Create a Budget That Reflects Your Priorities

A budget is not designed to restrict spending—it helps direct money toward what matters most.

Start by dividing expenses into categories such as:

- Housing

- Transportation

- Food

- Insurance

- Debt payments

- Savings

- Investments

- Entertainment

Tracking expenses each month can reveal opportunities to reduce unnecessary spending while increasing savings or investments.

Even small monthly improvements often produce meaningful long-term results.

3. Build an Emergency Fund First

Before taking additional investment risks, establish a financial safety net.

Unexpected expenses such as medical bills, home repairs, or temporary unemployment can create financial pressure.

An emergency fund covering three to six months of essential living expenses provides valuable flexibility and may reduce dependence on high-interest borrowing.

If saving several months of expenses feels overwhelming, begin with smaller, achievable milestones and increase the fund gradually.

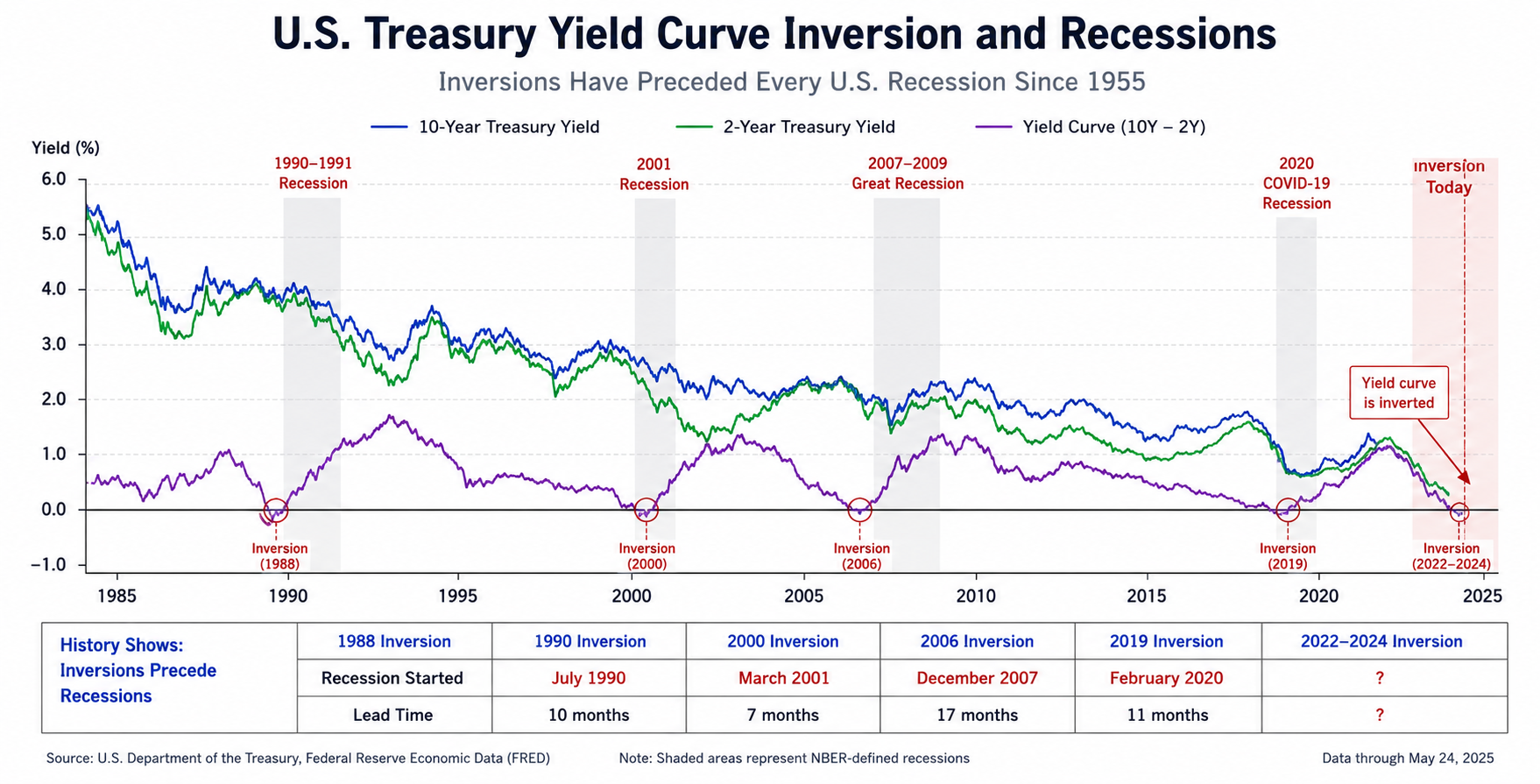

4. Invest With a Long-Term Perspective

Investment markets naturally experience periods of growth and decline.

Attempting to predict short-term market movements can be difficult even for experienced investors.

Many financial professionals recommend maintaining diversified investments while contributing consistently over time.

A disciplined, long-term approach often reduces emotional decision-making and allows compound growth to work more effectively.

Remember that all investments involve risk, including the possible loss of principal.

5. Eliminate Expensive Debt

High-interest debt can become one of the largest obstacles to financial progress.

Interest charges reduce the money available for saving and investing.

Prioritizing repayment of high-interest balances may improve financial flexibility and reduce future borrowing costs.

Many households use structured repayment methods, such as paying the highest-interest balance first or eliminating smaller balances to build momentum.

6. Diversify Your Sources of Income

Depending entirely on one paycheck may increase financial vulnerability.

Additional income sources can improve resilience during changing economic conditions.

Examples include:

- Freelance work

- Consulting

- Rental property income

- Dividend-paying investments

- Online businesses

- Selling digital products

- Educational services

Diversified income can help support savings goals while reducing financial uncertainty.

7. Increase Retirement Savings Gradually

Retirement planning becomes easier when contributions increase steadily over time.

Whenever income rises, consider directing part of each raise toward retirement savings before increasing discretionary spending.

Even small annual increases can produce meaningful long-term growth through consistent investing and compound returns.

Starting early provides additional time for investments to grow.

8. Continue Building Financial Knowledge

Financial education is an investment in itself.

Economic conditions evolve.

Tax rules change.

New financial technologies emerge.

Reading books, following trusted financial publications, attending educational seminars, or completing online courses can improve financial confidence and decision-making.

The more informed you become, the better prepared you are to adapt.

9. Review Your Financial Plan Every Year

Financial planning should evolve alongside your life.

Marriage, career changes, business opportunities, children, or retirement may all require adjustments.

An annual financial review allows you to evaluate:

- Budget performance

- Savings progress

- Investment allocation

- Insurance coverage

- Debt reduction

- Retirement contributions

- Long-term goals

Regular reviews help ensure your financial strategy continues supporting your changing priorities.

Common Money Habits That Support Long-Term Wealth

While everyone’s financial journey is unique, many financially successful households share similar habits:

- Spending less than they earn.

- Saving automatically every month.

- Investing consistently.

- Maintaining emergency savings.

- Avoiding unnecessary debt.

- Planning for retirement early.

- Reviewing finances regularly.

- Continuing financial education.

These habits may seem simple, but their cumulative impact over decades can be substantial.

Looking Toward the Future

Technology is rapidly changing the world of personal finance. Mobile banking, artificial intelligence, automated investing, budgeting applications, and digital payment systems are making financial management more convenient than ever.

However, no technology can replace the value of disciplined financial behavior.

Spend intentionally.

Save consistently.

Invest patiently.

Protect yourself from unexpected financial setbacks.

Continue learning throughout your life.

Financial independence is rarely achieved overnight. Instead, it develops through countless responsible decisions made over many years. Every budget you create, every dollar you save, and every thoughtful investment you make contributes to greater financial confidence and long-term security.

In an uncertain economic environment, your strongest financial advantage may not be predicting the future—it may simply be building habits that allow you to adapt, grow, and remain resilient regardless of what the economy brings next.