The “Soft Landing” Illusion? Why Smart Money is Betting on a 2026 Slowdown

The stock market is hovering near record highs, the unemployment rate remains historically low, and consumer spending, while cooling, hasn’t collapsed. On the surface, the US economy appears to have achieved the “soft landing” that policymakers have been desperately trying to engineer.

However, a closer look beneath the hood reveals a more complex and concerning picture. The “soft landing” narrative is facing a credibility crisis on Wall Street.

While the Dow Jones Industrial Average and the S&P 500 show resilience, a growing cohort of economists, fund managers, and corporate executives are quietly preparing for a “harder” landing than the consensus expects. The question for investors isn’t whether a recession will hit, but when and how deep it will be.

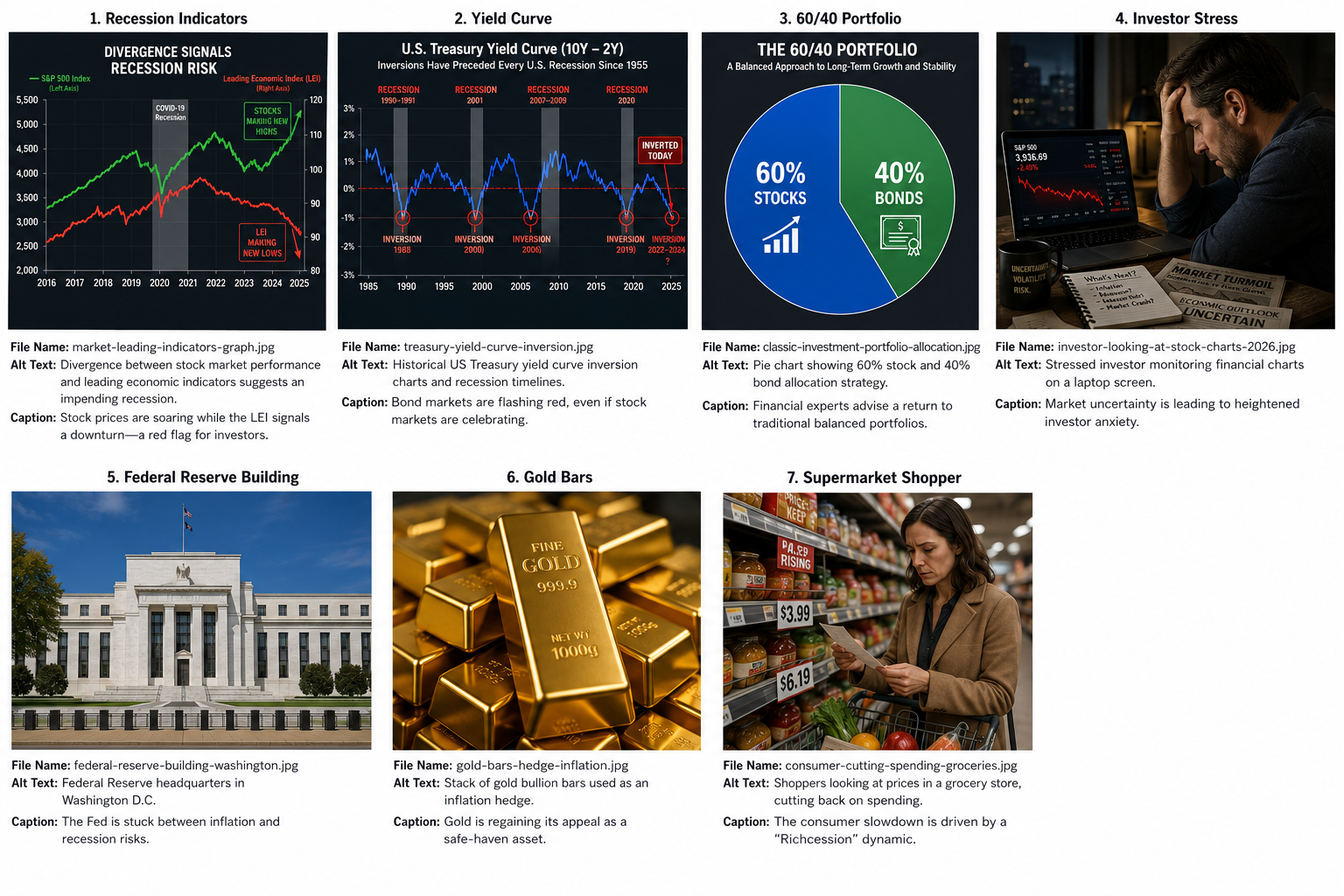

![Image 1]

Alt Text: Graph showing the divergence between the S&P 500 index and the Leading Economic Index (LEI), highlighting a recession warning signal.

Caption: The gap between stock prices and economic fundamentals is widening, a classic pre-recession signal.

The “Richcession” and the Weakening Consumer

One of the primary drivers of the current confusion is the bifurcation of the American consumer. We are seeing a phenomenon that some economists are calling a “Richcession”—where the economic slowdown is primarily being felt by lower and middle-income households, while higher-income individuals continue to spend.

Data from major retailers highlights this divide. Walmart and Target are reporting strong earnings, but they are also noting that consumers are trading down to cheaper brands and buying fewer discretionary items. Conversely, luxury brands like Hermès are still seeing robust demand.

This split is critical because consumer spending accounts for roughly 70% of US GDP. If the lower 80% of earners—who are feeling the pinch of depleted pandemic savings, rising credit card debt, and stubbornly high prices for essentials—start to cut back further, the “soft landing” could quickly skid off the runway.

The primary reason the stock market has remained buoyant is the Artificial Intelligence (AI) boom. The “Magnificent Seven” stocks (Apple, Microsoft, Nvidia, etc.) have driven the majority of the market’s gains over the past year. The market is pricing in a productivity miracle driven by AI.

The AI Hype vs. The Reality of Productivity

However, there is a growing concern that this is a bubble driven by promise rather than delivery. While AI is undoubtedly transformative, it is still in its early stages. For the stock market to justify its current valuations, companies need to show that AI is significantly boosting revenues and margins today, not just in 2030.

If corporate earnings fail to meet the sky-high expectations set by the AI narrative, the tech-heavy market could face a significant correction, dragging the broader economy down with it.

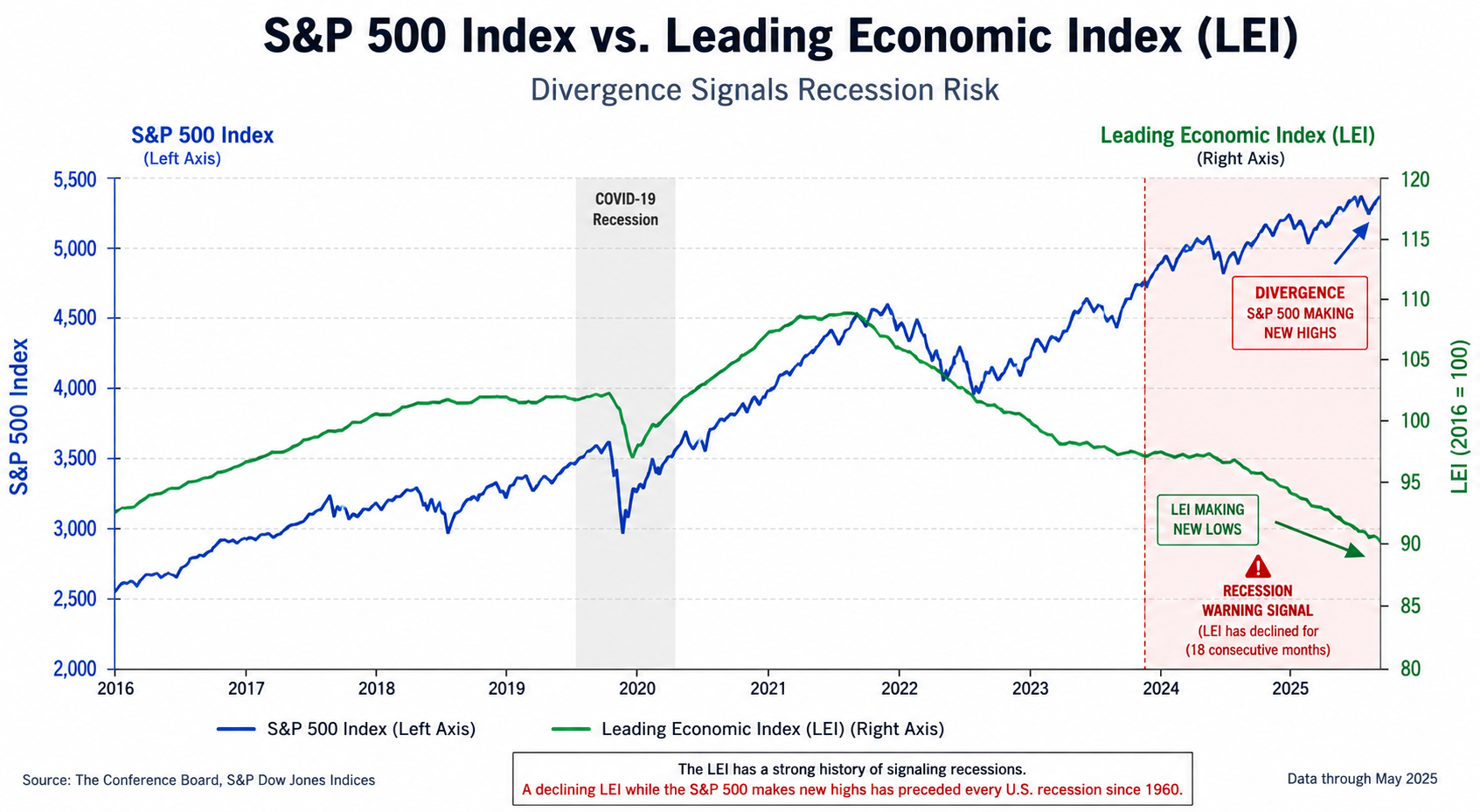

What the Bond Market is Saying (And Stocks Aren’t Listening)

Perhaps the most reliable recession indicator is the bond market, specifically the yield curve. The US Treasury yield curve has been inverted since 2022—meaning short-term interest rates are higher than long-term rates. Historically, an inverted yield curve has preceded every modern recession.

While it’s true that the economy hasn’t officially entered a recession yet, the lag time is longer than usual. The warning is clear. Equities are ignoring the bond market, but history suggests it is usually the bond market that is correct.

![Image 2]

Alt Text: US Treasury yield curve chart showing inversion and historical recession timing.

Caption: The yield curve remains inverted, a signal that has predicted every US recession of the last 50 years.

Expert Strategy: How to Position for Slowdown

Given the conflicting signals, how should investors prepare? We spoke to several financial strategists to get a consensus on the best plays for a “slowdown” scenario.

1. Prioritize Quality and Dividend Aristocrats

In a slowdown, cash flow is king. Investors should look for companies with strong balance sheets, low debt, and consistent cash flow. “Dividend Aristocrats”—companies in the S&P 500 that have increased dividend payouts for 25+ years—become particularly attractive. They provide a steady income stream that often holds up better than growth stocks during a downturn.

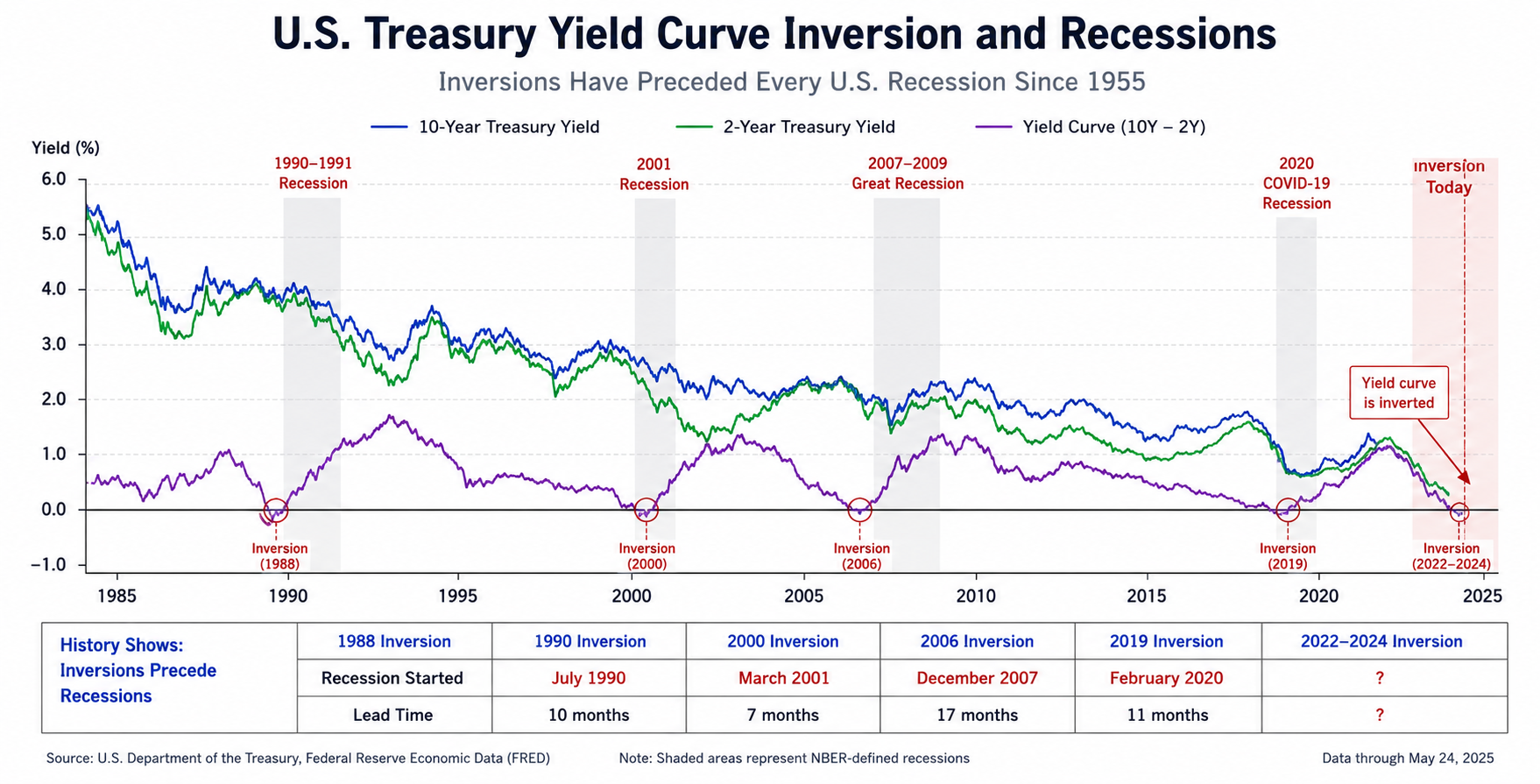

2. The 60/40 Portfolio is Back

For years, the classic 60/40 portfolio (60% stocks, 40% bonds) was considered dead. Low interest rates meant bonds didn’t provide the buffer they used to. However, with yields now above 4% on Treasury bonds, the 60/40 portfolio is back. It offers protection against equity volatility and a “risk-free” return that hasn’t been seen in over a decade.

3. Dollar Cost Averaging

The phrase “time in the market beats timing the market” is never more true than during a period of uncertainty. Trying to “sell at the top” is practically impossible. Strategists recommend sticking to a dollar-cost averaging strategy—investing a fixed amount of money at regular intervals—to smooth out the volatility.

![Image 3]

Alt Text: A portfolio pie chart illustrating a 60/40 asset allocation split between stocks and bonds.

Caption: The classic 60/40 portfolio is making a comeback as bonds offer attractive yields.

Opportunities in a Slowdown: Don’t Panic, Allocate

Just because a slowdown might be coming doesn’t mean investors should sell everything and go to cash. A slowdown creates opportunities.

- Utilities and Consumer Staples: These sectors are defensive. People need electricity, water, food, and medicine regardless of what the economy is doing. These stocks tend to be less volatile.

- Healthcare: Especially pharmaceuticals and insurance, which are typically recession-resistant.

- Gold: As a hedge against inflation and a safe-haven asset, gold often performs well when real interest rates fall or during geopolitical turmoil.

The Verdict: Proceed with Caution

The economic environment of 2026 is one of the most uncertain in recent memory. The data is noisy, and the market seems to be trading on “hope” rather than “data.” While an immediate crash is unlikely, a “soft-ish” landing or a mild recession in the second half of the year is becoming a base case scenario for many firms.

The Financial Takeaway:

- Check your debt: High-interest credit card debt is a wealth killer in a high-rate environment.

- Emergency Fund: Ensure you have 6–12 months of living expenses in a liquid high-yield savings account.

- Review your holdings: Are you overexposed to unprofitable tech companies? Rotate into cash-flowing assets.

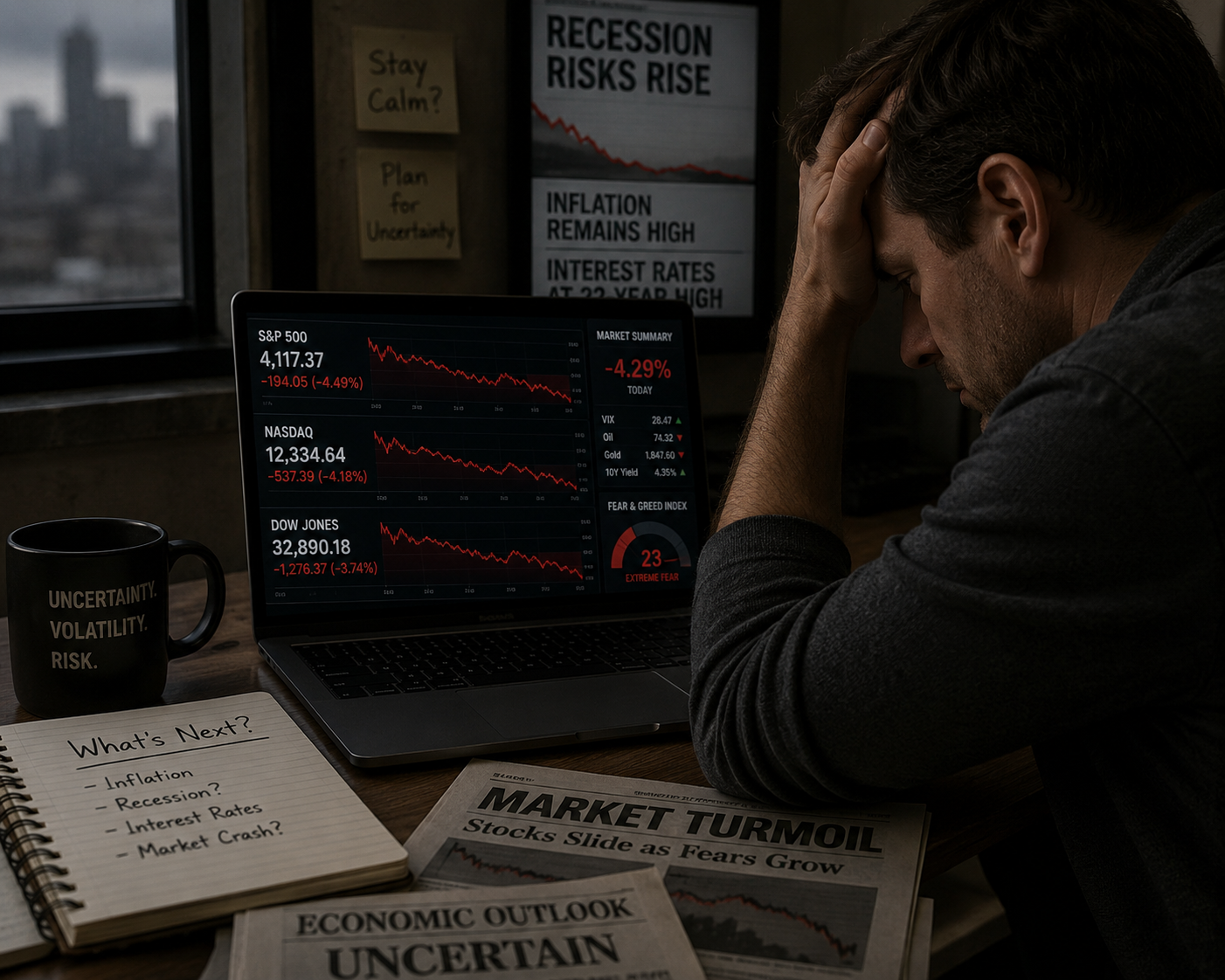

![Image 4]

Alt Text: An image showing a stressed investor looking at a laptop screen with stock charts, representing economic anxiety.

Caption: Investor anxiety is rising as recession fears persist alongside high market valuations.

The Central Bank Dilemma

The Federal Reserve is walking a tightrope. If they cut rates too soon, they risk inflaming inflation again. If they keep rates too high for too long, they risk breaking the economy.

Recent comments from Fed officials suggest they are in “wait and see” mode. They want to see inflation definitively move toward the 2% target before committing to cuts. However, the labor market is showing signs of softening, with the Job Openings and Labor Turnover Survey (JOLTS) showing fewer job openings.

This puts the Fed in a difficult position. The markets are pricing in rate cuts, but the data might not justify them yet. This discrepancy is likely to cause volatility in the coming months.

![Image 5]

Alt Text: Federal Reserve building in Washington D.C., representing monetary policy decisions.

Caption: The Federal Reserve faces a tough decision on interest rates as economic data sends mixed signals.

Conclusion: The New Normal

It’s time to accept that the days of zero-interest rates and massive fiscal stimulus are over. We are entering a new financial regime characterized by higher volatility and lower returns. “Buying the dip” may not be the winning strategy it was in the post-2009 era.

Instead, active management, tactical asset allocation, and a focus on income are set to win the day. The “soft landing” might be a mirage, but a well-prepared portfolio doesn’t rely on the weather—it relies on a solid ship.

[WORDPRESS UPLOAD DATA]

Title: The “Soft Landing” Illusion? Why Smart Money is Betting on a 2026 Slowdown (And How to Protect Your Portfolio)

Category:

- Finance (Primary)

- Market Analysis

- Investment Strategy

Tags:

- 2026 Economic Outlook

- Recession Prep

- Stock Market Volatility

- Federal Reserve

- Inflation

- AI Bubble

- Retirement Planning

- Asset Allocation

- 60/40 Portfolio

- Wealth Management

Featured Image Alt Text: Financial crisis concept with a wooden block tower falling, representing market instability in 2026.